3. Health Care Savings that are Tax-Free During Retirement

To understand the saving potential of an HSA, it may be helpful to think of it as another retirement account.

At Equity Trust, a self-directed HSA can complement your retirement accounts, providing another tax-advantaged vehicle to help you save and invest for your financial future – but with a specialized focus: health care.

In addition to helping save for health care expenses during retirement, it may also be possible to view your HSA similar to another Traditional IRA.

After you turn 65, funds distributed from an HSA for something other than qualified medical expenses are no longer subject to the 20-percent early distribution penalty and are only subject to ordinary income tax.

In essence, distributions for non-qualified medical expenses from an HSA after age 65 have the same tax treatment as funds in a Traditional IRA or 401(k). (See IRS Publication 969 for more information)

4. Health Care Savings that are Yours to Keep

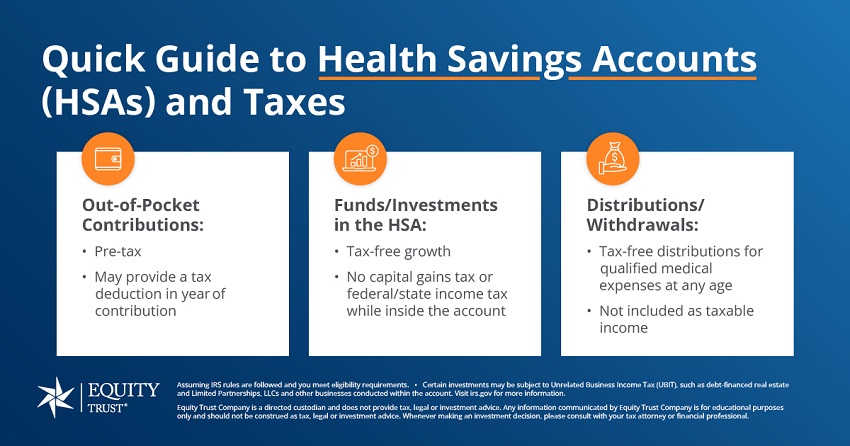

Unlike Flexible Spending Accounts (FSAs) and other medical savings accounts, HSAs are not “use-it-or-lose-it.” Account balances may be carried over from one tax year to the next.

You determine how much is contributed to your HSA each year (based on the contribution guidelines set by the IRS), and whether to pay current medical expenses from the account or save the money for future medical expenses.

It may also be possible to pay for medical expenses out-of-pocket when they are due, while saving all documentation and receipts so you can reimburse yourself with a tax-free distribution from your HSA at a later date.

There is no requirement to pay the medical expense directly with an HSA distribution – only that the distributed amount is for qualified medical expenses and is properly documented to the IRS and supported with receipts.

Let’s consider another hypothetical example where you saved all receipts, invoices, and supporting documentation for 10 years of qualified medical expenses – but never took an HSA distribution and paid them all out-of-pocket.

As long as the qualified medical expenses occurred after your HSA was established, it may be possible to reimburse yourself with a tax-free lump-sum distribution for the total amount, 10 years later.

Please consult with a tax attorney or financial professional and reference IRS Publication 969 and IRS Publication 502 before making any financial or investment decisions.

Finally, similar to an IRA, your HSA is entirely portable and stays with you even if you change jobs. However, if your new employer doesn’t offer a high-deductible health plan (or you decide to change plans and are no longer enrolled in a HDHP), you can no longer contribute to your HSA but can still invest your current funds.

5. Health Care Savings with Investment Freedom

Finally, a self-directed HSA at Equity Trust is more than a savings account.

Like all accounts at Equity Trust, you can invest your HSA in what you know best – whether it’s real estate, notes, private equity and a variety of alternative assets, or possibly traditional assets like stocks, bonds and mutual funds.

With an HSA at Equity Trust, you have the opportunity to build tax-free health care savings for you and your family – now and in the future.

1What types of accounts does Equity Trust hold?

Equity Trust holds a variety of IRAs, as well as other self-directed accounts, including:

- Traditional IRA

- Roth IRA

- SIMPLE IRA

- SEP IRA

- Solo 401(k)

- Roth Solo 401(k)

- Health Savings Account (HSA)

- Coverdell Education Savings Account (CESA)