Self-Directed Coverdell Education Savings Account

Empower your child's future with flexible, tax-advantaged savings

A Coverdell account is a valuable savings tool designed to help families save for educational expenses with tax advantages. Learn about the eligibility requirements for a Coverdell ESA, how a self-directed Coverdell ESA operates, and the steps to open an account.

X

Get started by choosing an option below.

Call an IRA Counselor

Schedule a Discovery Call

Access Coverdell Education

Savings Account Guide

What is a Coverdell Education Savings Account?

A Coverdell Education Savings Account, or CESA, is a trust or custodial account set up for paying qualified education expenses of a designated beneficiary. Contributions are made with after-tax dollars, and the earnings grow tax-free, provided they are used for qualified education costs such as tuition, books, and supplies. CESAs offer a flexible way to plan for a child’s education, from elementary through higher education, allowing for a variety of investments to potentially grow the savings.

While some refer to it as a Coverdell IRA, that’s actually a common misconception – this account is specifically designed for education savings, not retirement.

At Equity Trust Company, you can self-direct your CESA to invest in a broad range of asset classes, including real estate, precious metals, and more.

Video Resources

Benefits of a Coverdell ESA

Why do some investors choose a CESA to save for education costs? Here are some of the reasons:

Education savings: A Coverdell ESA allows parents or families to set aside funds that can grow tax-free, provided they are used for qualified education costs. This includes tuition, books, supplies, and sometimes even room and board. Starting a CESA early can maximize the benefits of compounding interest, creating a fund to support the educational needs of the beneficiary from elementary through higher education.

Tax advantages: Contributions in a CESA are made with after-tax dollars and not tax-deductible, but the earnings grow tax-free within the account. Distributions from a CESA are also tax-free, provided they are used for qualified education expenses such as tuition, books, supplies, and other related costs.

Transferability: Funds in a CESA must be used by the designated beneficiary by age 30 or they will be subject to taxes and penalties in case of withdrawal. However, the funds in the account can be transferred to a different ESA to be used by or for a different qualified family member.

Investment flexibility: In addition to traditional investment opportunities, with a qualified custodian, you can expand your portfolio into alternative investments. This flexibility enables you to potentially enhance your returns while managing risk, ensuring that your educational savings grow effectively over time.

Interested in alternative investments but don’t know where to start?

No problem. We make it easy to locate potential investments.

Available through our online account management system, myEQUITY, the WealthBridge portal provides a secure, direct connection to alternative asset investment platforms.

Discover Wealthbridge Our online marketplace introduces you to dozens of asset providers across various investment types including turnkey real estate, private equity, cryptocurrency, precious metals, and more.

Visit Investment DistrictContribution Limits for a CESA

Currently, contributions for a Coverdell ESA are capped at $2,000 per year, per child. You can contribute for the year all the way up until that year’s tax deadline.

For more CESA information, see IRS Publication 970.

CESA Contribution Limits, Eligibility Requirements, and Contribution Deadlines

| 2026 | 2025 | |

| Standard Limit (up to age 18) | $2,000 | $2,000 |

| Contribution Deadline | 4/15/2027 | 4/15/2026 |

| Modified AGI Limits to Qualify for Account – Single | $95,000 – $110,000 | |

| Modified AGI Limits to Qualify for Account – Married Filing Jointly | $190,000 – $220,000 | |

HSA Contribution Limits, Eligibility Requirements, and Contribution Deadline

| 2026 | |

| Standard Limit (up to age 18) | $2,000 |

| Contribution Deadline | 4/15/2027 |

| Modified AGI Limits to Qualify for Account – Single | $95,000 – $110,000 |

| Modified AGI Limits to Qualify for Account – Married Filing Jointly | $190,000 – $220,000 |

Coverdell ESA Eligibility Requirements

A CESA can be established for a beneficiary under the age of 18 or for an individual with special needs. A parent, grandparent, or other relative can open the account and designate the beneficiary. Once the account is opened, contributions can be made by anyone, including the beneficiary, parents, grandparents, relatives, and even corporations or organizations.

It is not required to have earned income to make contributions to a CESA.

Coverdell ESA Rules

Understanding the rules that govern a CESA is key to making the most of this powerful tool for funding your child’s education.

Contribution limits: While the annual contribution limit is $2,000, these contributions can be made by multiple sources per year, such as individuals, relatives, or outside organizations. However, the total contributions must not exceed the annual limit. The same is true if the beneficiary has multiple accounts; contributions must not exceed $2,000.

Income limits: Eligibility to contribute to a Coverdell Education Savings Account (CESA) is subject to income limits. If your income exceeds certain thresholds, you may not be eligible to contribute to a CESA. Learn more about income limits here.

Age requirements: The beneficiary must be under the age of 18 when the account is established, except for those with special needs. Funds must be used by the time the beneficiary is 30, or they will face taxes and penalties when withdrawing funds.

Qualified expenses: To maintain tax-free status, CESA funds must be used for qualified educational expenses. These include tuition, fees, books, supplies, and equipment required for enrollment at eligible institutions. This covers primary, secondary, and higher education, including vocational schools. Room and board are also qualified if the beneficiary is enrolled at least half-time in a postsecondary institution.

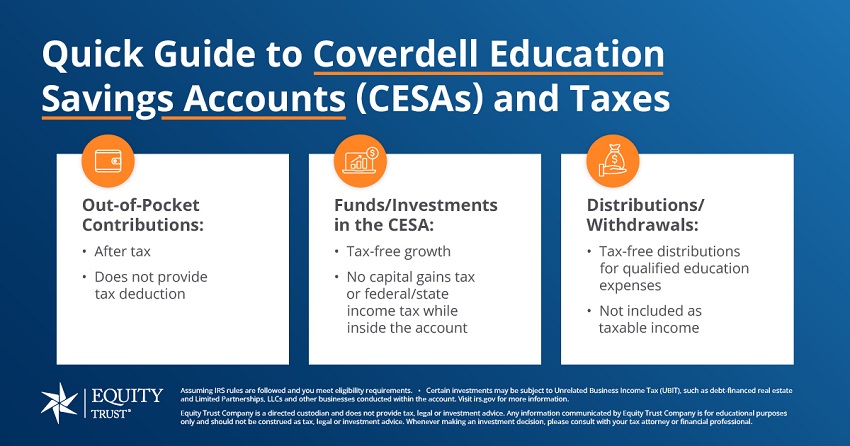

CESA and Taxes

Contributions to a Coverdell ESA are made with after-tax income and are not tax deductible. The contributions, however, can then grow tax-free through potential profits from your investments like interest, dividends, or capital gains. When money is withdrawn to pay for qualified education expenses, it’s tax-free.

CESA and Withdrawals / Distributions

Distributions from a CESA are tax-free if used for qualified education expenses at eligible institutions. However, tax-free educational assistance like scholarships can affect this. If distributions exceed adjusted qualified expenses or are used for non-qualified expenses, they may be taxable and subject to a 10% penalty. For detailed rules, refer to IRS Publication 970.

CESA vs. 529 Plans: A Comparison

When it comes to saving for education, there are several account options available to help you plan for the future. Two of the most popular choices are the Coverdell ESA and the 529 plan. Both offer unique benefits and can play a vital role in funding your child’s education.

Here’s a chart that breaks down the key differences between the Coverdell ESA and the 529 plan, so you can determine which might be the best fit for your family’s needs.

| CESA | 529 | |

| Tax Advantages | Tax-free growth and withdrawals for qualified expenses | Tax-free growth and withdrawals for qualified expenses |

| Beneficiary Transfer | Account can be transferred to another family member of the beneficiary | Account can be transferred to another family member of the beneficiary |

| Contribution Limits | Annual contribution limits are capped at $2,000 per child | No federal limits on contributions; however, different states can set their own limits |

| Qualified Expenses | Can cover both K-12 and higher education tuition and expenses like books, fees, and supplies | Covers higher education tuition and expenses, apprenticeship and homeschool expenses, and student loan repayment |

| Penalties for Early Withdrawal | Earnings will be taxed as income plus 10% penalty on earnings | Earnings will be taxed as income plus 10% penalty on earnings |

| Investment Options | Open to both public (stocks, bonds, etc.) and with a qualified custodian, private (real estate, crypto, private equity, etc.) investments | Limited to the preset options offered by state |

| Age Restrictions | Cannot contribute to the account once the beneficiary reaches 18, and funds must be used by 30 | Most states have no age restrictions on when funds must be used |

| Income Limits | If your modified adjusted gross income exceeds $110,000 for single filers or $220,000 for joint filers, you are not eligible to contribute | No income limits |

| CESA | |

| Tax Advantages | Tax-free growth and withdrawals for qualified expenses |

| Beneficiary Transfer | Account can be transferred to another family member of the beneficiary |

| Contribution Limits | Annual contribution limits are capped at $2,000 per child |

| Qualified Expenses | Can cover both K-12 and higher education tuition and expenses like books, fees, and supplies |

| Penalties for Early Withdrawal | Earnings will be taxed as income plus 10% penalty on earnings |

| Investment Options | Open to both public (stocks, bonds, etc.) and with a qualified custodian, private (real estate, crypto, private equity, etc.) investments |

| Age Restrictions | Cannot contribute to the account once the beneficiary reaches 18, and funds must be used by 30 |

| Income Limits | If your modified adjusted gross income exceeds $110,000 for single filers or $220,000 for joint filers, you are not eligible to contribute |

Getting Started with a CESA

Here are the three steps to getting started with an Equity Trust self-directed Coverdell ESA:

Open your Equity Trust CESA

One of our specialized IRA Counselors can assist you, or you can do it online through our account management system myEQUITY.

Fund your new tax-advantaged account

There are three ways to fund your account: rollover, transfer, or out-of-pocket contribution.

Choose your investment and direct Equity Trust to send funds

Our myEQUITY team will walk you through submitting your investment online. One of will be assigned to assist you if you need help.

FAQs

Where can you open a Coverdell Education Savings Account?

Are Coverdell contributions tax deductible?

Are Coverdell distributions taxable?

Is a Coverdell a 529 plan?

Can a Coverdell be rolled into an IRA?

What can Coverdell account funds be used for?

Can a Coverdell be used to pay student loans?

Can a Coverdell be used for room and board?

What happens to unused Coverdell funds?

Do Coverdells have an age limit?