Self-Directed Solo 401(k)

Support your future with a Solo 401(k) designed for your business and retirement needs.

A Solo 401(k) is a retirement savings option for self-employed individuals or small business owners, offering high contribution limits, tax advantages, and flexible investment options. Take control of your retirement by investing in traditional and alternative assets. Learn how to maximize your savings and secure your financial future with a Solo 401(k).

X

Get started by choosing an option below.

Call an IRA Counselor

Schedule a Discovery Call

Access The Ultimate Guide

to the Solo 401(k)

What is a Solo 401(k)?

A Solo 401(k), also known as an Individual 401(k), is a retirement plan designed specifically for self-employed individuals or small business owners with no full-time employees, aside from a spouse. This plan offers the same benefits as a traditional 401(k), including tax-deferred growth and the ability to make substantial contributions each year, but it is tailored for individuals running their own businesses.

What sets the Solo 401(k) apart is that it allows you to contribute both as an employee and as an employer, maximizing your retirement savings potential. The plan provides significant flexibility with contribution limits and offers features like tax advantages and loan options that can benefit self-employed individuals looking for greater control over their retirement planning.

Videos

Benefits of a Solo 401(k)

High contribution limits: Solo 401(k) plans allow for higher contribution limits compared to traditional retirement accounts, enabling you to contribute both as an employee and an employer. This flexibility helps maximize your retirement savings potential.

Loan options: Solo 401(k) participants can borrow from their account, offering financial flexibility. Loans must be repaid with interest, typically within five years, without penalties if the rules are followed.

Spousal contributions: If your spouse is employed by your business, they can also contribute to a Solo 401(k), allowing for doubled contributions and greater retirement savings for your household.

Profit-sharing contributions: As both the employer and employee, you can make profit-sharing contributions up to 25% of your compensation, further increasing the amount you can contribute to your retirement each year.

Discover the Equity Solo 401(k) Solution

Looking for a Solo 401(k) with more control, less complexity, and built-in features designed for real investors?

Our platform offers:

- All-in-one system to establish, manage, and maintain your plan

- Direct control of funds for real-time investing

- Lightning-fast transactions, including Roth conversions

- IRS-ready forms (5500-EZ, 1099-R) auto-generated for easy filing

- Fully integrated banking with Fortis for faster funding and investment reconciliation

Unlike many solutions, we don’t just give you plan documents. We give you a complete recordkeeping and transaction system, built for both traditional and alternative investments.

Interested in alternative investments but don’t know where to start?

No problem. We make it easy to locate potential investments.

Available through our online account management system, myEQUITY, the WealthBridge portal provides a secure, direct connection to alternative asset investment platforms.

Discover Wealthbridge Our online marketplace introduces you to dozens of asset providers across various investment types including turnkey real estate, private equity, cryptocurrency, precious metals, and more.

Visit Investment DistrictSolo 401(k) Contribution Limits

The IRS establishes annual contribution limits for a Solo 401(k), which include both employee salary deferrals and up to 25% of your compensation for the pre-tax profit-sharing portion. Additionally, there is a maximum compensation limit that can be used when calculating the allowable contributions.

Discover the current year’s contribution limits.

Solo 401(k) Contribution Limits and Deadlines

| 2026 | 2025 | |

| Standard Contribution Limit – Employee Salary-Deferral Contribution | $24,500 | $23,500 |

| Standard Contribution Limit – Employee Salary-Deferral & Employer Profit-Sharing Contributions * | $72,000 | $70,000 |

| Catch-up Contribution Limit (Age 50 and older) – Employee Salary-Deferral Contribution | $32,500 | $31,500 |

| Catch-Up Contribution Limit (Age 50 and older) – Employee Salary-Deferral & Employer Profit-Sharing Contributions * | $80,000 | $77,500 |

| Super Catch-Up Contribution Limit (Age 60 – 63) – Employee Salary-Deferral | $35,750 | $34,750 |

| Super Catch-Up Contribution Limit (Age 60 – 63) – Employee Salary-Deferral & Employer Profit-Sharing Contributions * | $83,250 | $81,250 |

| Contribution Deadline | 12/31/2026 | 12/31/2025 |

* The annual limit for the Employer Profit-Sharing Contribution is 25% of the employee’s pay (20% of pay for a self-employed person)

| 2026 | |

| Standard Contribution Limit – Employee Salary-Deferral Contribution | $24,500 |

| Standard Contribution Limit – Employee Salary-Deferral & Employer Profit-Sharing Contributions * | $72,000 |

| Catch-up Contribution Limit (Age 50 and older) – Employee Salary-Deferral Contribution | $32,500 |

| Catch-Up Contribution Limit (Age 50 and older) – Employee Salary-Deferral & Employer Profit-Sharing Contributions * | $80,000 |

| Super Catch-Up Contribution Limit (Age 60 – 63) – Employee Salary-Deferral | $35,750 |

| Super Catch-Up Contribution Limit (Age 60 – 63) – Employee Salary-Deferral & Employer Profit-Sharing Contributions * | $83,250 |

| Contribution Deadline | 12/31/2026 |

* The annual limit for the Employer Profit-Sharing Contribution is 25% of the employee’s pay (20% of pay for a self-employed person)

Solo 401(k) Eligibility Requirements

A Solo 401(k) is designed for both incorporated and unincorporated businesses, including sole proprietorships, partnerships, and corporations. To contribute, you must receive a salary or wage from self-employment.

The business entity cannot have any employees other than the owner’s spouse. In a partnership, the only employees permitted are the self-employed partners and their spouses.

Additionally, the Solo 401(k) must be the only retirement plan maintained by the business. The plan must be established by the last day of the business’s tax year to allow employee salary deferral contributions for that year, while employer contributions can be made up until the business’s tax filing deadline, including extensions.

Solo 401(k) Account Rules

Required minimum distributions: Once you reach age 73, you must take minimum distributions (RMDs) from your Solo 401(k). The amount of your RMD is based on several factors, like account balance and is subject to income tax.

Loan restrictions: Loans from a Solo 401(k) must follow IRS guidelines. The maximum loan amount is typically 50% of your account balance, up to $50,000. If loans are not repaid within the required time frame, they may be subject to taxes and penalties.

Plan deadlines: To make contributions for the current year, your Solo 401(k) plan must be established by the last day of your business’s tax year, typically December 31. Employee salary deferrals must also be made by this date, while employer contributions can be made up until your tax filing deadline.

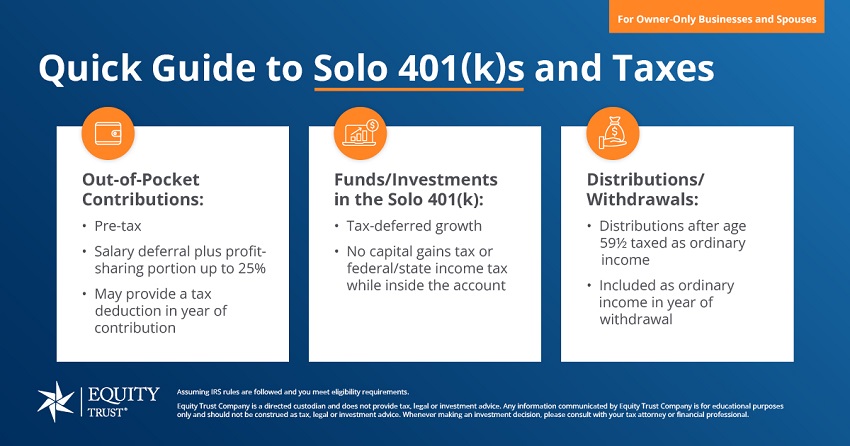

Solo 401(k) and Taxes

Contributions to a Solo 401(k) are made with pre-tax dollars, allowing you to reduce your taxable income in the year the contributions are made. This provides an immediate tax benefit, as your savings grow tax-deferred. While funds remain within the account, investment earnings are not subject to capital gains or federal and state income taxes.

Distributions from a Solo 401(k) are taxed as ordinary income when withdrawn, typically after reaching age 59½. If you withdraw funds before 59½, those distributions may be subject to income tax and an additional 10% early withdrawal penalty unless exceptions apply.

Required minimum distributions (RMDs) begin at age 73. The tax-deferred nature of the Solo 401(k) allows your investments to grow more effectively over time, maximizing your retirement savings potential.

Solo 401(k) vs. Roth Solo 401(k) Comparison

As self-employed individuals and small business owners look toward retirement, deciding which retirement plan works best for them is important. Both a Solo 401(k) and a Roth Solo 401(k) offer distinct tax strategies and withdrawal guidelines, making them powerful tools depending on your financial goals.

The following comparison chart highlights the major differences between these two options. Keep in mind that with the Equity Solo 401(k) solution, you can take advantage of both options, within the same plan.

| Traditional Solo 401(k) | Roth Solo 401(k) | |

| Tax Advantages | Contributions are tax-deductible, and withdrawals are taxed in retirement | Contributions are after-tax and withdrawals are tax-free in retirement |

| Contribution | Allows both employee and employer pre-tax contributions | Allows both employee and employer pre-tax contributions, but employee deferrals are after-tax; employer contributions are pre-tax |

| Required Minimum Distributions | RMDs start at age 73 | No RMDs |

| Profit-Sharing Contributions | Up to 25% of compensation is tax-deductible for the business | Employer contributions are pre-tax and taxed when withdrawn |

| Penalties for Early Withdrawal | Earnings will be taxed as income plus 10% penalty on earnings | Earnings will be taxed as income plus 10% penalty on earnings |

| Tax Treatment at Withdrawals | Withdrawals are taxed as ordinary income in retirement | Withdrawals are tax-free if requirements are met |

| Eligibility | Self-employed individuals or business owners with no employees, except a spouse | Self-employed individuals or business owners with no employees, except a spouse |

| Traditional Solo 401(k) | |

| Tax Advantages | Contributions are tax-deductible, and withdrawals are taxed in retirement |

| Contribution | Allows both employee and employer pre-tax contributions |

| Required Minimum Withdrawals | RMDs start at age 73 |

| Profit-Sharing Contributions | Up to 25% of compensation is tax-deductible for the business |

| Penalties for Early Withdrawal | Earnings will be taxed as income plus 10% penalty on earnings |

| Tax Treatment at Withdrawals | Withdrawals are taxed as ordinary income in retirement |

| Eligibility | Self-employed individuals or business owners with no employees, except a spouse |

Getting Started with a Solo 401(k)

Here are the steps to get started with your Equity Solo 401(k):

Confirm your eligibility

Make sure you have self-employment income and no full-time employees other than yourself or your spouse.

Obtain your Employe Identification Numbers (EINs)

You’ll need two: one for your business and one for your Solo 401(k) plan. Both can be obtained through the IRS website.

Complete your application online

Gather your ID, EINs, and business details to finish the application and start your subscription.

Open your bank account

Use our integrated bank or your preferred provider to establish your 401(k) bank account.

Fund your plan & start investing

Contribute or roll over funds, then invest directly through your plan with your connected bank account.

FAQs

Who can open a Solo 401(k)?

Can I convert an Individual 401(k) to a Roth 401(k)?

Is a Solo 401(k) tax-deductible?

Can you have a Solo 401(k) and an employer 401(k)?

Can an S-corp have a Solo 401(k)?

What makes the Equity Solo 401(k) platform different?

Do Solo 401(k)s require a third-party custodian to hold plan assets and assist with investment transactions?

How do I invest with checkbook control?

Can I move my existing Solo 401(k) into Equity’s platform?

Can I invest in real estate, private placements, or crypto?

Can I make Roth contributions and conversions?

Can I use my 401(k) as collateral for a loan?

Do employer 401(k) contributions show on W-2?

Equity Specialty Services, LLC (“ESS”) has partnered with SEPira(k) to offer you the Equity Solo 401(k) solution to establish and manage your Solo 401(k). By combining SEPira(k)’s technology platform with ESS’s customer support, you will have the tools to manage your Solo 401(k) seamlessly.

Equity Specialty Services, LLC is a services company which offers services such as acting as a solo 401k solution provider, offering document preparation and referral loans services and other services to assist an investor with his/her investments. Equity Specialty Services does not offer investment, tax, or legal advice, and no services offered by us should be considered to replace the need for qualified investment, tax, and legal professionals. It is for education only. Please consult your legal or financial advisor before making any financial decisions. Equity Specialty Services may receive or give referral fees from third party vendors for services it offers to investors.