Introduction: Why condos are in the spotlight in 2025

From the ripple effects of the deadly condo collapse in Surfside, Florida, to a massive storm surge from multiple hurricanes, and record-high insurance premiums, the 2025 condominium market represents a pivotal moment for real estate investors. Across the Sunbelt and coastal regions, aging buildings, mounting regulations, and shifting buyer behavior are redefining the asset class.

What was once a relatively stable and affordable entry point into real estate investing is now a terrain requiring strategic awareness. For investors, understanding the risks and evaluating investment potential through the lens of compliance, cost burden, and market saturation is more critical than ever.

This report unpacks the major forces reshaping the condo landscape, with a deep dive into Florida and Texas—two markets experiencing some of the most dramatic changes in inventory, pricing, and regulatory pressure.

A market in flux: The condo landscape from the ground up

Inventory is climbing, but sales aren’t

Altos Research shows a sharp rise in active condo inventory over the past 12 months:

In Florida, inventory rose from 54,142 in June 2024 to 74,241 in June 2025—a 37% increase.

Texas saw a 17% inventory jump over the same period, now at 12,229 condos.

Nationwide, active condo inventory climbed 35%, from 163,506 to 221,213.

This inventory surge suggests more than seasonal fluctuation. In many regions, it’s the result of owners exiting aging or high-cost buildings, motivated by fear of special assessments, high HOA dues, and declining property values.

But while listings have grown, sales have not kept pace:

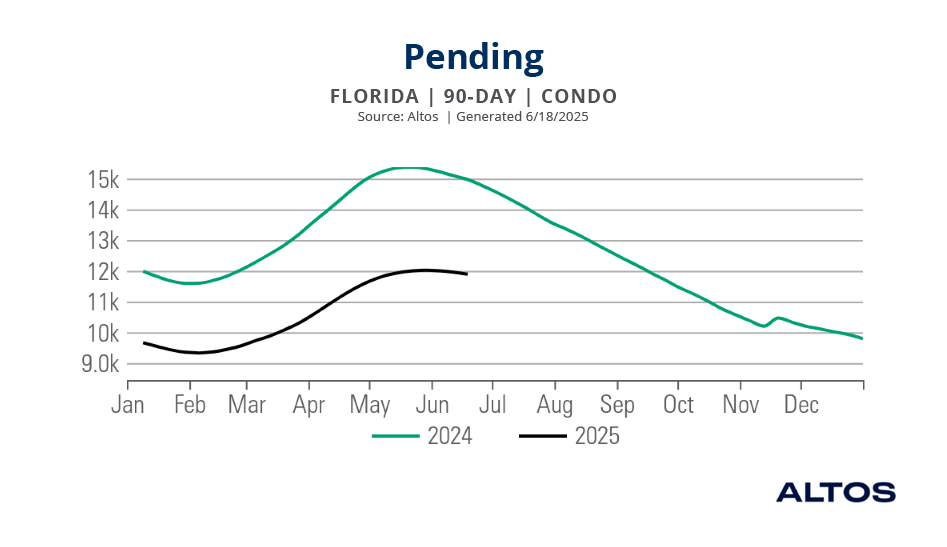

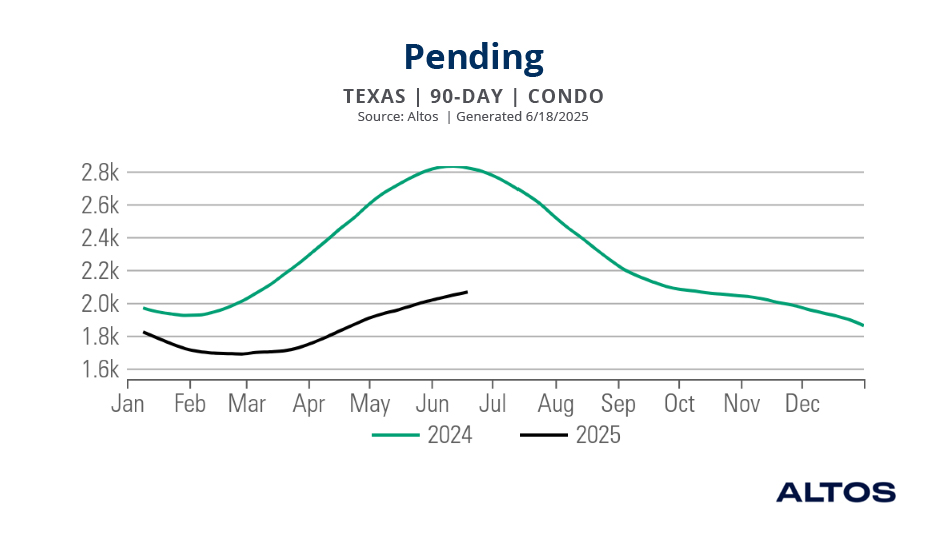

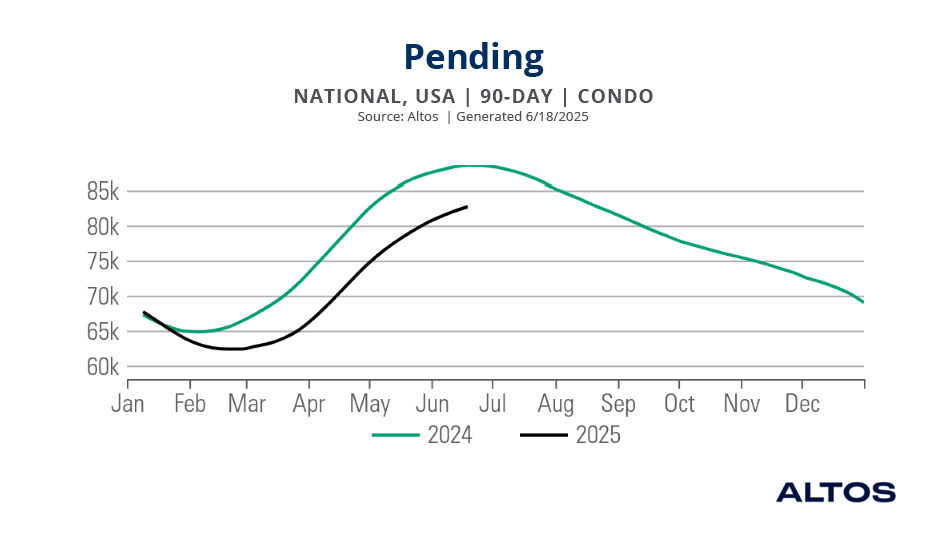

Pending sales in Florida dropped 21% YoY (15,094 in June 2024 vs. 11,887 in June 2025).

Texas pending sales fell even further—down 27%, from 2,832 to 2,065.

National pending condo sales decreased 6.7%, signaling broad buyer hesitation.

For real estate investors, this divergence may mean opportunity—but only with rigorous due diligence. In this type of buyer’s market, knowing how to assess building condition, reserve health, and long-term cost outlook is essential to protecting your investment.

Concentration of unsold inventory: Florida’s dominance

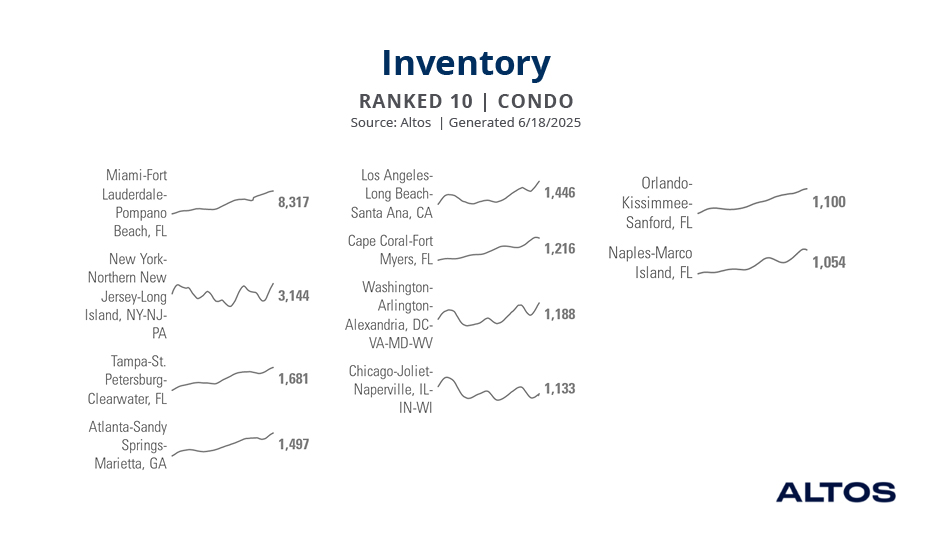

As of June 18, 2025, Altos Research data reveals that among the top 10 U.S. metro areas with the highest number of unsold condos on the market, Miami–Fort Lauderdale–Pompano Beach leads the nation with 8,317 active condo listings. More telling is that half of the top 10 metro areas with the most unsold condo inventory are located in Florida.

This isn’t just a Florida issue—it’s a Florida-centric crisis.

What this suggests is a concentrated oversupply in markets that were once the crown jewels of condo investing. Whether due to aging infrastructure, soaring insurance premiums, or unfavorable legislation, demand has not kept up with new listings in these areas. And as more owners list units in a rush to exit before special assessments or reserve funding requirements take hold, inventory continues to pile up.

For investors, regional overexposure presents both a warning and an opportunity. In saturated metros, distressed sellers may be open to steep discounts—but the due diligence burden is higher than ever. Condo docs, reserve studies, insurance binders, and structural inspection records must all be reviewed through a long-term cash flow lens.

Price volatility and the “correction by tier”

Condo prices in Florida are experiencing clear downward pressure, but it’s not uniform.

Top 25% of Listings:

Peaked at $1.3M in April 2022

June 2025: $869,000

Down 33%

Secondary Tier:

Peaked at $550,000 in June 2022

Now: $435,000

Down 20.9%

Entry Level:

Peaked at $199,900 in July 2022

Now: $175,000

Down 12%

The market is correcting most aggressively at the top. The highest tier, which historically relied on cash buyers and international investors, has become increasingly illiquid as these buyers pivot to newer construction or less regulatory risk.

Pending sale prices reflect this shift:

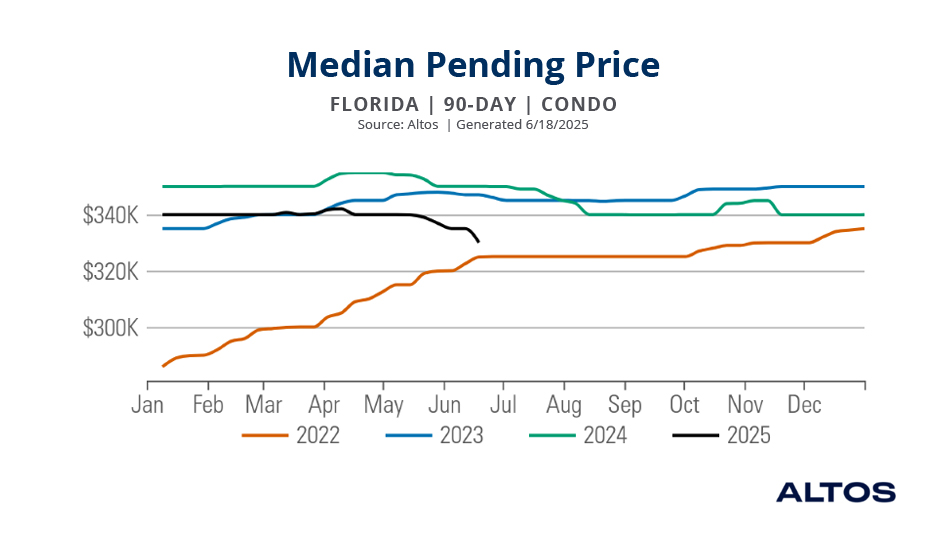

Median pending price for Florida condos fell from $350,000 in June 2024 to $330,000 in June 2025 (-5.7% YoY).

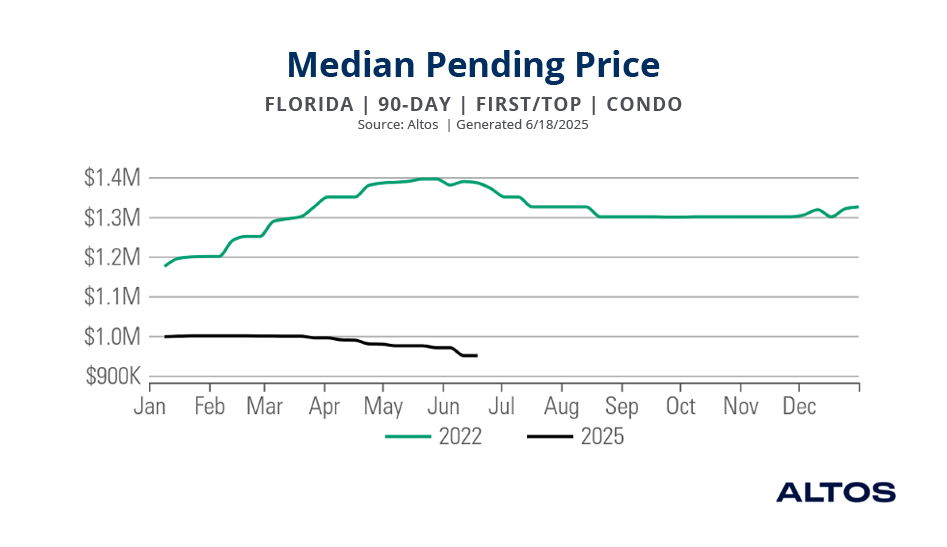

Top-tier pending contracts saw a sharper decline—from $1.39M in June 2022 to $950,000 in June 2025 (-32%).

Meanwhile, sellers are resisting these trends. The median list price in June 2025 is $345,000, not far off its 2022 peak. However, nearly 43% of Florida condo sellers reduced their prices in June 2025, up from just 17% in 2021—a 153% increase. In Texas, 36% of listings saw reductions, up from 13% in 2013 (+177% over 12 years).

For investors, this means one thing: leverage. Sellers—especially in older buildings—are motivated. But that doesn’t automatically mean a good deal. Deep inspection of financials, reserves, insurance coverage, and compliance status is essential.

Investors can also use our Real Estate Investing Hub, with data reports and other resources for wherever you are in your investment journey.

Regulatory shifts and insurance pressures

The Surfside effect: new laws, new costs

In 2021, Champlain Towers South, a condo building in Surfside, Florida, partially collapsed, possibly due to construction flaws and structural degradation, resulting in the deaths of 98 residents. Following the collapse, the state of Florida passed laws in 2022 requiring:

Milestone structural inspections at 30 years (or 25 if near the coast)

Fully funded reserves by 2025

According to the CRC Group, nearly 600,000 of Florida’s 1.4 million condos are over 40 years old. Yet as of mid-2025, fewer than 25% of condo associations have confirmed compliance.

Insurance: A market under stress

Insurers have responded by increasing scrutiny:

Carriers now demand higher insurance-to-value ratios

Policies often require detailed structural histories and completed inspections

Florida premiums have doubled in the past 6–9 months, according to Seneca Insurance and the Insurance Information Institute

More than 1,400 condo buildings in Florida are on Fannie Mae’s “blacklist,” making them ineligible for conventional financing. As mortgage options dry up, prices soften further—and cash becomes king.

Spotlight: Insurance carriers are becoming stricter

Seneca Insurance Company has highlighted the Surfside tragedy as a turning point in the habitational insurance landscape. Their August 30, 2022 report emphasized several key changes:

The Champlain Towers South property had only $31.4 million in insurance coverage across 136 units—far below replacement cost.

Carriers have since intensified focus on insurance-to-value and property inspections.

Older buildings must now undergo structural analysis and produce detailed maintenance records to secure coverage.

Florida and California have been most affected by premium hikes, due in part to hurricanes, wildfires, and hail losses.

Seneca noted that many master condo policies have doubled in cost since late 2023. As a result, many associations are turning to layered insurance strategies and the Excess & Surplus lines market.

Seneca’s takeaway: insurers are not only pricing in physical risk—but governance risk. Poorly run associations without proper maintenance plans or documentation are being penalized in pricing or denied coverage entirely. Read more at SenecaInsurance.com.

This has two implications for investors:

Due diligence on insurance coverage is non-negotiable.

Uninsured or underinsured properties carry both financial and legal exposure.

This 21-story building was once considered a luxury staple. One couple paid $490,00 for their unit and spent an additional $100,000 to renovate it. Now, each owner faces a $134,000 special assessment, their part in a $30 million proposal by the condo board to pay for repairs like a roof replacement and facade waterproofing. But those who can’t afford it are having trouble selling, with some units selling for as low as $110,000—a price driven by steep repair costs and stalled financing.

One retired couple purchased a golf course-view condo for $319,000 in 2021. In two years:

Insurance doubled

HOA dues rose to $1,000/month

A $7,200 special assessment hit

43 units in their gated community were for sale

They accepted an offer for $358,500, well below asking

What seemed like a tax-advantaged retirement investment turned into a forced exit.

Implications for investors: The risk of “unknowable” expenses

Condos come with communal obligations. If an association has waived reserves or delayed maintenance, future costs fall on all unit owners. That can affect cash flow, tax strategy, and asset value.

Liquidity and lending challenges

Many investors use financing to purchase real estate. But if a property becomes blacklisted or uninsurable, financing becomes impossible—and resale becomes uncertain.

Investment math has changed

Let’s say you purchase a $400,000 condo and expect $2,200 in monthly rent. After standard costs, you might project a 5.5–6% cap rate.

Now factor in:

A $25,000 surprise special assessment

$3,600 annual insurance premium hike

Your ROI could drop below 4%, while your liquidity is tied up in an illiquid and depreciating asset.

Investing within a SDIRA

Self-directed IRAs can put investors in a better position for these types of investments because they can use their retirement funds to invest with cash, rather than relying on financing that may be difficult to obtain.

Alternative approaches

Newer condos and proactive HOAs

Targeting buildings constructed in the last 20 years with:

No waivers of reserves

Documented maintenance

Recent structural reports

Build-to-rent communities

For income-focused investors, build-to-rent homes in suburban growth markets offer:

Predictable maintenance costs

Full landlord control

Less exposure to communal financial risk

Self-Directed IRAs

Investors who have the cash in their retirement account can leverage it to purchase condos, sidestepping the need for financing. Using a self-directed IRA, investors can purchase the property outright and use it to grow their retirement savings.

Looking ahead

Condo investing in 2025 requires deeper diligence and strategic flexibility. That’s why researching potential markets and reviewing all data is essential for investors looking to add condos to their portfolio.

Explore free market-specific data powered by Altos Research, and more, at the Weekly Real Estate Report section here. To view condo data in your area, add your ZIP code and a report will be generated. Once on the report page, you can switch from single-family home to condo market data.

Real estate market data throughout this guide is sourced from Altos Research unless otherwise noted.

Equity Specialty Services, LLC is a services company which offers services such as document preparation services, IRA Power Loans services and other services to assist an investor with its investments. Equity Specialty Services, LLC is not authorized to advise you as to which documents you should use or may need or which services are recommended. Equity Specialty Services, LLC does not offer investment, tax, or legal advice, and no services offered by us should be considered to replace the need for qualified investment, tax, and legal professionals. Please consult your legal or financial advisor before making any financial decisions. Under the guidelines for legal document preparation services, you must make all legal decisions yourself — including decisions about the type of documents you need. Equity Specialty Services, LLC may receive or give referral fees for services it offers to investors.

Join over 100,000 subscribers who receive investing and wealth-building news and education in their inbox.

You are leaving trustetc.com to enter the ETC Brokerage Services (Member FINRA/SIPC) website (etcbrokerage.com), the registered broker-dealer affiliate of Equity Trust Company. ETC Brokerage Services provides access to brokerage and investment products which ARE NOT FDIC insured. ETC Brokerage does not provide investment advice or recommendations as to any investment. All investments are selected and made solely by self-directed account owners.