With the rising cost of education, a Coverdell Education Savings Account (CESA) can be a powerful tool to help combat education expenses, potentially reduce dependence on financial aid, and receive tax benefits. Understand how a CESA works, eligibility, how you can grow your CESA and more to see if this account may be right for you.

1. What is a Coverdell Education Savings Account (CESA)?

A Coverdell ESA is an account set up for paying qualified education expenses for a designated beneficiary, according to the IRS.

2. How does a self-directed CESA work?

Equity Trust offers a self-directed CESA, which allows you to invest in almost any asset, tax free or tax deferred, while saving for education costs. Investing funds contributed to a CESA may potentially lead to the overall growth of the account, in a tax-advantaged fashion.

Many Equity Trust clients are primarily investing in alternative assets, beyond traditional stocks, bonds and mutual funds. Some of these alternatives include real estate, private lending, promissory notes, tax liens and many others.

A Self-Directed CESA Case Study

Brian opened Coverdell accounts for each of his four children. He saw the savings potential: money saved in a CESA can be withdrawn tax-free when used for qualified education expenses.

An active real estate investor, Brian decided to try to grow his children’s accounts using self-directed CESAs.

A CESA’s annual contribution limit is $2,000. Brian was concerned that it would take a while to build up enough capital in the account to be able to invest in real estate. His purchasing power increased when he learned that he could partner with other self-directed accounts to make investments.

Brian thought it would be difficult to find a suitable investment property for less than $50,000 in the city of Nashville, but before long he found a vacant lot in the city for $8,000.

He partnered three of his children’s self-directed CESA accounts to purchase the lot. One child’s CESA invested $4,000, and his two other children’s CESAs each invested $2,000.

Brian saw potential in the lot because he spotted new housing construction nearby, as well as a mobile home park that was on the market.

“As I reviewed the potential of the area, I believed the value was going to change once they sold that mobile home park,” Brian recalls. “Once the mobile home park sold, additional houses were built continuing to push values up.”

The land was sold 60 days later for $60,000. The sale proceeds returned the CESA accounts in the same proportion as was used for the purchase.

Brian had been investing in real estate for a while before he was aware that he could self-direct his retirement account, CESA or other accounts into real estate and other alternative investments.

Between his and his wife’s retirement accounts and his children’s CESAs, Brian’s family now has a total of eight accounts at Equity Trust.

Video: Coverdell Education Savings Account FAQs

3. What can a Coverdell Education Savings Account be used for?

A CESA can be used to fund qualified education expenses recognized by the Department of Education through an accredited institution.

According to IRS Publication 970, the expenses can be either qualified for higher education expenses or qualified elementary and secondary education expenses.

Some examples of qualified education expenses may include tuition, room and board, books, supplies, equipment, uniforms, software, academic tutoring, special needs services, and others.

The contribution limit for a Coverdell Education Savings Account is $2,000 per year, per child (i.e. beneficiary).

According to the IRS, there may be a reduced limit depending on your MAGI. If your MAGI is between $95,000 and $110,000 (between $190,000 and $220,000 if filing a joint return), the $2,000 limit for each designated beneficiary is gradually reduced. If your MAGI is $110,000 or more ($220,000 or more if filing a joint return), you can’t contribute to anyone’s Coverdell ESA.

A common question is, “Can I set up a CESA for my child or grandchild and then have an aunt or uncle set up a CESA, or other relative and have each person contribute 2,000?”

Regardless of the number of CESAs opened for the beneficiary the maximum contribution per year, per beneficiary is $2,000, until the child (beneficiary) reaches the age of 18, even if you have more than one contributor. There are some exceptions to those rules for special needs beneficiaries.

5. Are contributions to a Coverdell Education Savings Account tax-deductible?

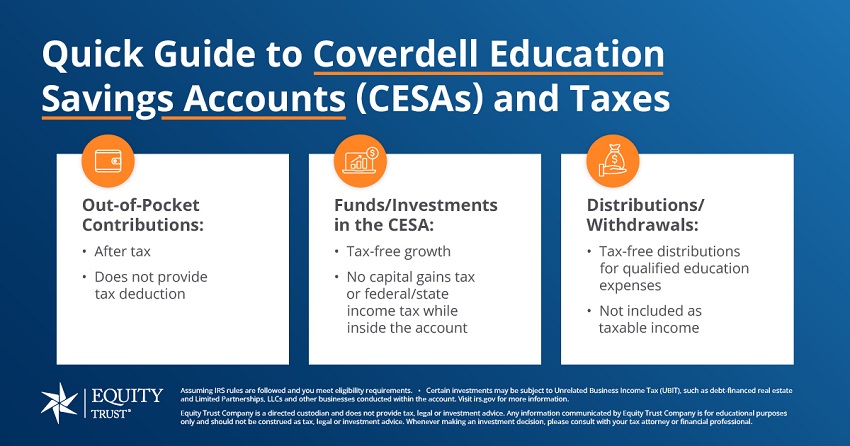

No – Contributions to a CESA are not tax deductible. Individuals contribute to a Coverdell ESA with after-tax dollars, but those contributions can then grow tax-free through potential profits from the investments that you’re making. When money is withdrawn to pay for qualified education expenses, it’s tax-free.

6. Are there income limits associated with CESAs?

Yes – There are what’s referred to as Modified Adjusted Gross Income (MAGI) limits.

If you’re single in 2023, and you make between $95,000 and $110,000 MAGI, you can only make a partial contribution to a CESA account. This is what’s referred to as the phase-out range. As you get closer to that $110,000, you can only put a small fraction of the full $2,000 allowable limit on an annual basis.

Once your income is over $110,000, unfortunately you cannot contribute to a child or grandchild, or other family member’s Coverdell ESA.

If you’re married and filing jointly, and your MAGI is between $190,000 and $220,000 the contribution limits decrease and as you reach $220,000, you cannot contribute to a CESA.

Visit the IRS website for worksheets to help you determine MAGI and contribution limits.

7. When must assets be distributed from the account?

Assets must be distributed when the beneficiary turns 30 (rule doesn’t apply to a special-needs beneficiary).

If there’s a balance in the CESA at the time the beneficiary reaches age 30 or dies (if earlier), it must be distributed within 30 days. A portion representing earnings on the account will be taxable and subject to the additional 10-percent tax.

The beneficiary may avoid these taxes by rolling over the full balance to another beneficiary who is under the age of 30.

8. What’s the difference between a 529 savings plan and a Coverdell Education Savings Account?

Typically, with a 529 plan you get a tax deduction for making contributions to the plan, however, you’re restricted on the types of investments you can make with the funds.

Whereas with a Coverdell ESA, you can invest in just about anything as long as your following the rules and regulations associated with other self-directed accounts.

Can I have both a 529 and a Coverdell Education Savings Account?

Join over 100,000 subscribers who receive investing and wealth-building news and education in their inbox.

You are leaving trustetc.com to enter the ETC Brokerage Services (Member FINRA/SIPC) website (etcbrokerage.com), the registered broker-dealer affiliate of Equity Trust Company. ETC Brokerage Services provides access to brokerage and investment products which ARE NOT FDIC insured. ETC Brokerage does not provide investment advice or recommendations as to any investment. All investments are selected and made solely by self-directed account owners.