The self-directed Roth Solo 401(k) (also known as the Roth Individual 401(k)) is available to anyone with a Solo 401(k). It’s a benefit to higher-paid employees and self-employed individuals who may have been excluded from having a Roth IRA because of income limitations.

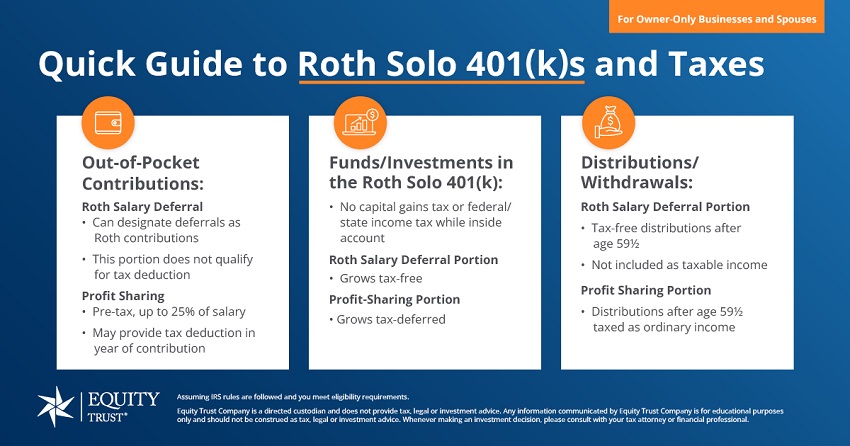

The Roth Individual 401(k) possesses the same benefits of the Individual 401(k) (higher contribution limits than other accounts), with the tax benefits of the Roth IRA. The contribution limits are the same as the Individual 401(k), but you can designate your contributions through salary deferral as Roth contributions.

Ultimate Self-Directed Solo 401(k) Guide

Discover all you need to know about the powerful tool that allows small business owners and sole proprietors to contribute, deduct, and invest nearly 10 times the amount they could with other retirement accounts.

Potential Benefit of the Roth Individual 401(k): Higher Contribution Limits

In 2024 you can annually contribute up to $23,000 – or up to $30,500 if you’re 50 or over – through salary deferral. Plus, you can contribute a profit-sharing portion (0-25%) of your salary. In 2024 the limit from both sources is $69,000 ($76,500 if you are 50 or over).

Like the Individual 401(k), the Roth Individual 401(k) is for incorporated and unincorporated businesses, sole proprietorships, partnerships, and corporations. The only requirement for contributions to this plan is that you receive a salary or wage.

The business entity must have no additional employees other than the spouse of the proprietor—or, in the case of a partnership, the only employees must be self-employed partners and their spouses.

An Individual 401(k) plan must be the only arrangement maintained by the business that is not included as part of a controlled group under federal tax law.

Deadline

The deadline for establishing an Individual 401(k) plan is the last day of your business’s tax year (December 31, for a calendar tax year).

However, if your business is incorporated, you may want to establish an Individual 401(k) plan early in the tax year to make employee salary deferrals based on the Form W-2 income throughout the year.

This is necessary because you may not defer on compensation that is paid to you from your corporation before you establish the Individual 401(k) plan.

What Makes a Roth Solo 401(k) Self-Directed?

When a Roth Solo 401(k) is referred to as a self-directed account, it simply means you can use the account invest in areas outside of the traditional stocks and bonds. That’s the primary difference between a self-directed and traditional retirement account — where you put those investment dollars.

With a self-directed Roth Solo 401(k) or IRA, you can invest in a variety of areas, including:

Real estate

Private debt like corporate debt offerings, notes secured by deeds of trust or mortgages

Private equity-like stock of C-corporations, limited partnerships, LLCs and REITs

Precious metals, including gold, silver, platinum, and palladium

Cryptocurrency like Bitcoin

If you’re interested in opening a self-directed Roth Solo 401(k), or for more information about this plan, please contact a Senior Account Executive at 855.233.4382.

Self-Directed Solo 401(k) FAQs

In this session, you’ll learn about:

Self-Directed Solo 401(k)s and Your Investment Options

Contributing to a Solo 401(k) and the Contribution Limits

Solo 401(k) Eligibility

Solo 401(k) Rules and Regulations

Potential Advantages of a Solo 401(k) or Roth Solo 401(k)

Let’s talk about your financial future.

Schedule a one-on-one session with an expert alternative investment counselor. We’re here to answer any questions, help guide you through the process, and provide more detailed information and education specific to your journey.

By entering your information and clicking Start a Conversation, you consent to receive reoccurring automated marketing text messages and emails about Equity Trust’s products and services. This consent is not required to obtain products and services. If you do not consent to receive text messages and emails from Equity Trust and seek information, contact us at 855-233-4382. Reply STOP to opt out from text messages. Message and data rates may apply. View Terms & Privacy.

You are leaving trustetc.com to enter the ETC Brokerage Services (Member FINRA/SIPC) website (etcbrokerage.com), the registered broker-dealer affiliate of Equity Trust Company. ETC Brokerage Services provides access to brokerage and investment products which ARE NOT FDIC insured. ETC Brokerage does not provide investment advice or recommendations as to any investment. All investments are selected and made solely by self-directed account owners.

By entering your information and clicking Get Started, you consent to receive reoccurring automated marketing text messages and emails about Equity Trust’s products and services. This consent is not required to obtain products and services. If you do not consent to receive text messages and emails from Equity Trust and seek information, contact us at 855-233-4382. Reply STOP to opt out from text messages. Message and data rates may apply. View Terms & Privacy.