What to Know

Certain investment strategies or investment types could trigger Unrelated Debt-Financed Income (UDFI) and could require an IRS Form 990-T. Equity Trust is here to help you complete this requirement. Need more info? Read on to learn more about this tax and the reporting requirements.

Watch to learn more about UBIT and UDFI and how Equity Trust can help with reporting:

LET US PREPARE YOUR 990-T

To assist you in meeting filing requirements, Equity Trust Company offers Form 990-T preparation and IRS required electronic payments to our clients for their IRAs.

What to Do

To avoid a $75 late-documentation penalty, Equity Trust requires your response to our notice. Please indicate your UBTI responsibility and chosen course of action by clicking one of the options below. If you’re still unsure, see the Frequently Asked Questions further down the page or email us at [email protected].

To view the associated fee schedule, click here.

Investments That Commonly Trigger UBTI

- Debt-financed property

- Investments into leveraged funds and/or partnerships

- Investments into operating businesses structured as LLCs

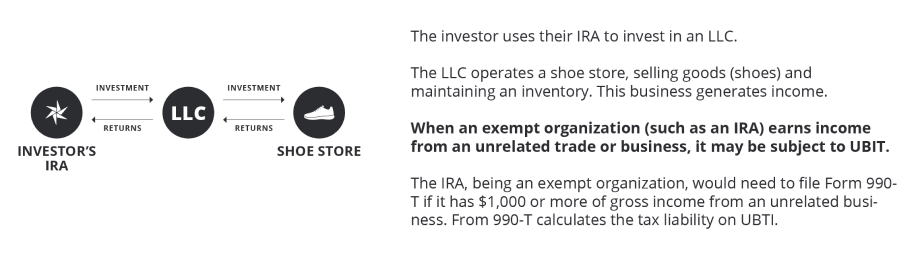

EXAMPLE ONE: UNRELATED BUSINESS INCOME TAX

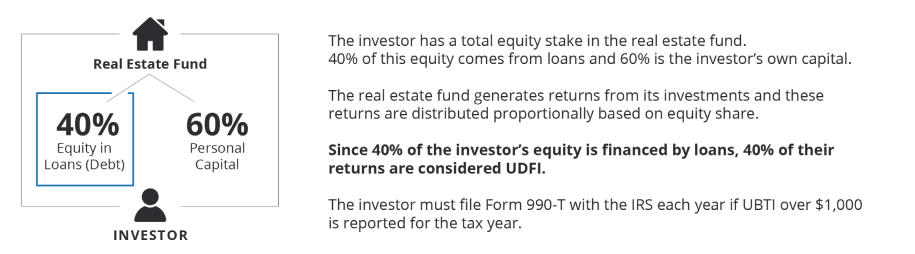

EXAMPLE TWO: DEBT-FINANCED INCOME

Frequently Asked Questions

What is Unrelated Business Income Tax (UBIT)?

UBIT, or Unrelated Business Income Tax, is levied on tax-exempt organizations for income generated from activities unrelated to their tax-exempt purpose. In the case of IRAs, this tax may apply when investing in an operating trade or business structured as a passthrough entity such as an LLC or LP. This tax is meant to eliminate competitive advantages.

What is Unrelated Debt-Financed Income (UDFI)?

UDFI, or Unrelated Debt-Financed Income, is a tax that is applied to leveraged investments, particularly real estate. It taxes earnings attributable to the leveraged portion. UDFI can apply to both directly owned properties that contain a mortgage, and investments in funds or partnerships.

Are UDFI and UBIT the same?

Although they are related concepts, Unrelated Debt-Financed Income is the activity that would result in the income produced, Unrelated Business Taxable Income (UBTI.)

How can I determine if UBIT or UDFI applies to my investment?

For an LP/LLC that generates a K1: Indications that UBIT was reported, resulting in a need for a 990-T, can be identified by looking at your investment(s) K1 partnership return:

- If Box 20 contains code “V”

- If the K1 has no Box 20 “V” but has positive amounts in Box 1, Box 2 and Box 10 shows liabilities, it’s best to consult with the investment issuer as UBIT may have been reported

For an IRA-owned investment property: If your investment property was leveraged during the tax year, resulting in income attributable to the leveraged portion exceeding $1,000, you’ll likely need to file a Form 990-T. Use our calculator for assistance.

What is defined as an operating business?

For purposes of UBIT, an operating business typically involves conducting active income-generating operations by offering goods or services and/or holding an inventory. Examples would include restaurants and stores.

If I owe tax, how is that paid?

The IRS requires that all UBIT/UDFI liability is to be paid from your IRA, not with personal funds. To submit a payment to the IRS from your Equity account, follow these easy steps:

myEQUITY: Money Movement > Bill Pay, click Launch Bill Payment Wizard

Midland360: need steps

Investors must pay any tax liability or make prepayments by April 15, 2025 for the 2024 tax year. This liability is paid from the IRA. Investors have to October 15, 2025 to file their 990-T if they’ve filed an extension for their IRA.

Please keep in mind that the 990-T filing and extension process will not impact the timing of your personal tax return.

What are the current tax rates?

The IRS provides the tax rates in its 990T preparation publication.

What if I don’t have my K1 yet?

It’s common for K-1s to reach investors close to the tax filing deadline, or even after. Many investors prepay any expected liability and file an extension to allow for more clarity. Filing an extension for your IRA will not impact the timing of your personal tax return.

What if I sold my property, or plan to sell it?

If you’ve sold your property during the tax year, you will still be required to file a 990-T.

If you haven’t yet sold your property, consider the advantages of a 1031 exchange to defer any UDFI liability.

What if the property is owned by my Real Estate Checkbook IRA, LLC?

Leveraged real estate owned within an LLC is treated the same as real estate owned directly in the IRA.

Will filing an extension impact my personal tax return timing?

No, your IRA would file an extension to allow you to gather the necessary items related to your 990-T by October 15. Remember, once April 15 passes, you’ve missed your opportunity to file an extension. Let us help you file an extension. (Link to “Help” landing page)