If you’re relatively young, the thought of saving for retirement might be the last thing on your mind when it comes to financial priorities. You may be dealing with car payments, mortgages, student loans, children… the list goes on. If you’re not already saving for retirement, you might want to consider starting. Here’s why.

Why You Should Save for Retirement

1. You Can’t Rely on Social Security

There’s a general rule of thumb that you’ll need 70 percent of what you make at the peak of your career in retirement. This 70 percent mainly deals with your standard of living, such as budget for food, entertainment, living costs, etc. In addition to this, you need to be prepared for unexpected expenses individuals don’t always plan for, such as medical bills or long-term care as you get older.

In the past, many Americans’ retirement plans consisted solely of Social Security. However, in the next 15 years alone, the ability to rely on this form of income in retirement will diminish.

According to the 2020 annual report of the Social Security Board of Trustees, the trust funds that disburse retirement, disability and other Social Security benefits will be depleted by 2035.

It’s also worth noting, “The coronavirus pandemic could also have a significant impact on the system’s long-term finances, as large-scale job losses cut into the payroll tax revenue that largely funds Social Security” according to AARP.

Even if Social Security isn’t completely gone by the time you retire, you will more than likely need an extra 30 to 40 percent of that 70 percent to live comfortably.

2. Achieve Your Retirement Goals

While some people find they have fewer expenses in retirement with children moved out and loans paid off, it’s important to consider what your retirement goals entail when it comes to saving for retirement. You might want to travel the world, start a small business from a hobby, purchase a second home on a beach or in the mountains, for example.

When you start saving for retirement at a young age, you potentially allow yourself to have a wider array of options in retirement to achieve these goals and dreams. The sky can be the limit if you start saving early.

3. The Numbers Make Sense

Without getting into the nitty-gritty of it, saving for retirement in a tax-advantaged account is a great way to grow your funds in general.

In general, if you contribute to a retirement account:

- The amount of taxes you owe on income decreases

- The earnings you make on your investments can either defer or avoid taxes

- Compound interest can be a powerful thing

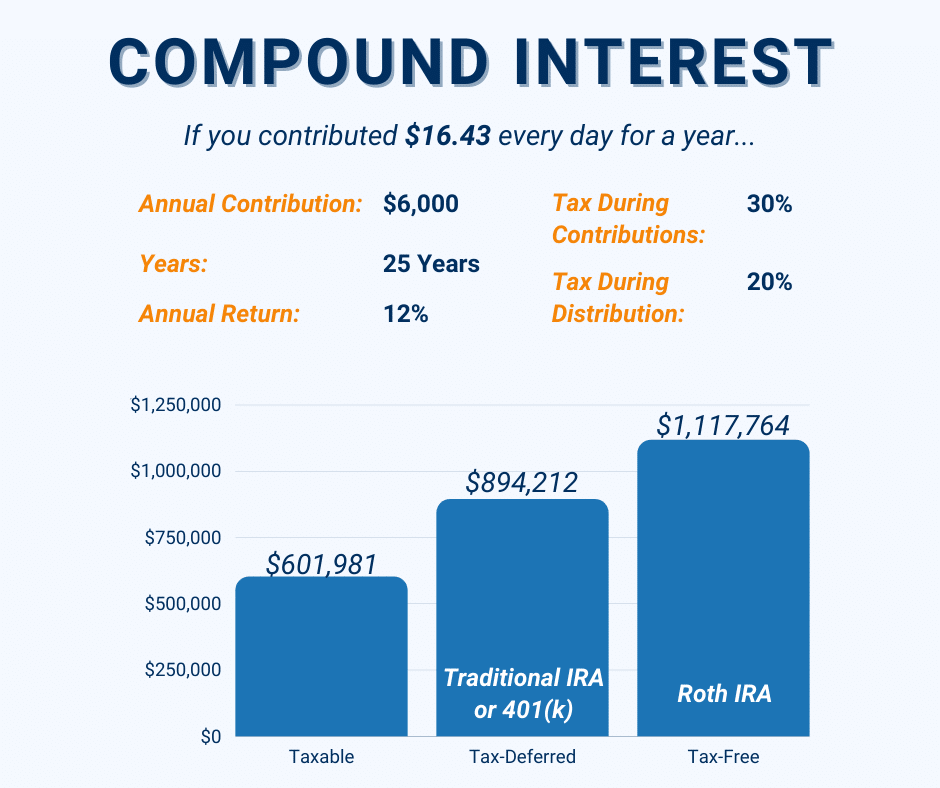

4. Compound Interest

Compound interest can be powerful, so powerful it can stand alone as a reason to start saving for retirement.

Here’s a short example to illustrate the power of compound interest: