Investing in retirement usually involves a bit of strategy, which a team of financial advisors can help with. One topic the advisors will probably discuss is investing in tax-free accounts vs. tax-deferred plans.

What’s the difference and how does it affect retirement investments?

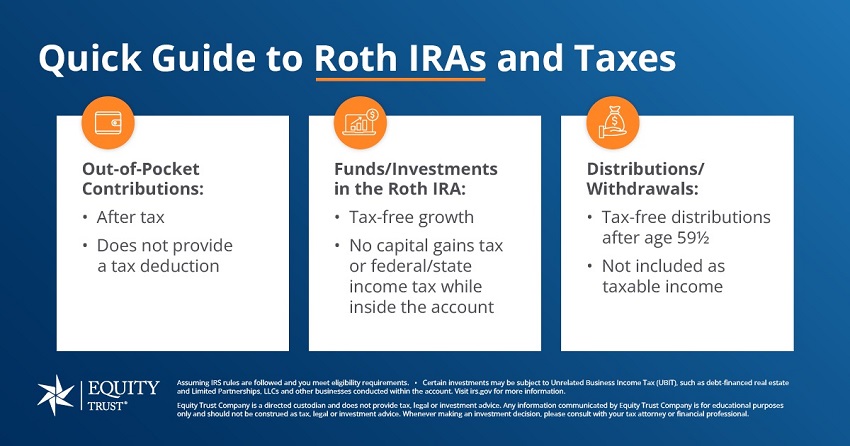

Tax-Free Plans

The money earned in the accounts will be tax free when withdrawn, as long as specific conditions are met. Common tax-free accounts include Roth IRAs, 529 College Savings Plans and Coverdell education savings accounts.

The money initially deposited into these accounts occurs post taxes, and these accounts are not included in income tax deductions. As the accounts earn interest, that interest will not be taxed when withdrawn according to the stipulations of the account.

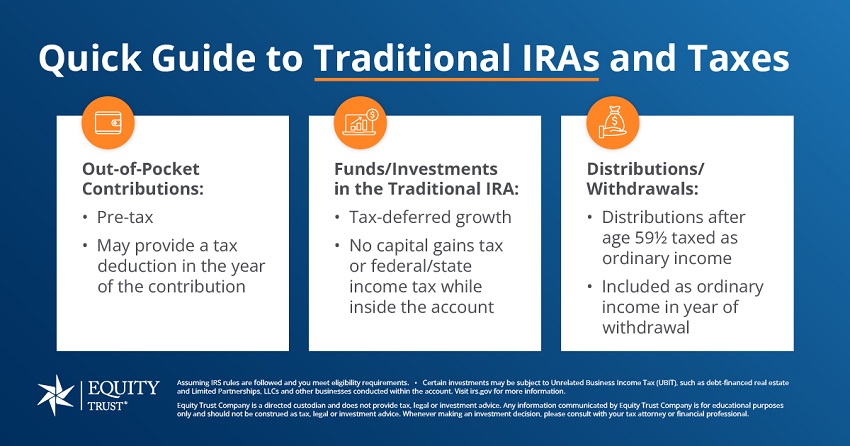

Tax-Deferred Plans

These accounts will require the investor to pay taxes on the money withdrawn from the accounts, but not on the money earned through the investment each year.

Common types of tax-deferred accounts include Traditional IRAs and 401(k)s – typically offered as employer-sponsored retirement plans. Sometimes these accounts allow investors to contribute money through the employer prior to it being taxed as well.

Because the money in these accounts can accumulate without taxation, investors often have a goal to grow the money in the account faster.

It’s Possible to Move from Tax-Deferred to Tax-Free

When transferred, there will be taxation on the money coming from the tax-deferred account; however, it will be at the current tax prices and the current amount being transferred.

The thought is that once in the tax-free account, the money will continue to grow (as it did in the tax-deferred account), but when withdrawn at a later date, taxes will not have to be paid on a larger amount at a potentially higher tax rate.

Equity Trust holds a variety of IRAs, as well as other self-directed accounts, including:

Traditional IRA

Roth IRA

SIMPLE IRA

SEP IRA

Solo 401(k)

Roth Solo 401(k)

Health Savings Account (HSA)

Coverdell Education Savings Account (CESA)

2

What are the advantages of opening a self-directed IRA?

Some advantages of self-directed IRAs include:

Tax-deferred or tax-free profits

Investment diversity (it is possible to invest in an array of assets in your retirement account)

Potentially building wealth for future beneficiaries

3

When I roll over funds from an employer-sponsored or qualified retirement plan, do they need to go directly into a traditional IRA?

No. Per IRS guidelines, rollovers from a qualified plan can be rolled over into a traditional or Roth IRA. If the rollover is made directly to the Roth IRA, the transferred amount is subject to income taxation but avoids the 10-percent early distribution penalty. You should consult with your plan administrator regarding the permissible withdrawal options allowed under the tax-qualified plan.

Join over 100,000 subscribers who receive investing and wealth-building news and education in their inbox.

You are leaving trustetc.com to enter the ETC Brokerage Services (Member FINRA/SIPC) website (etcbrokerage.com), the registered broker-dealer affiliate of Equity Trust Company. ETC Brokerage Services provides access to brokerage and investment products which ARE NOT FDIC insured. ETC Brokerage does not provide investment advice or recommendations as to any investment. All investments are selected and made solely by self-directed account owners.