Mark: You know, the payment wizard in myEQUITY. It is very easy to use.

Now. There’s some bumps in the roads that I had to begin. Mostly, when do you do it?

When do you do it and how do you do it?

Meaning, like I had an HVAC contractor that came in and did a whole new system. And I had a check overnighted to him and he received it on Friday and the job was supposed to be completed on Friday, but they didn’t finish it until Saturday.

And everyone knows you kind of hate paying a contractor before the job’s actually completed. Now, what I have done since then, and what I’ve learned, is I’ll actually still have the check made out to the correct parties, the correct individual. Then I’ll hand the check to the contractor when it’s done. And I’ll send it all overnight to myself, so I have it.

By using the Bill Pay system in myEQUITY, you can do exactly that and just have the check sent to you.

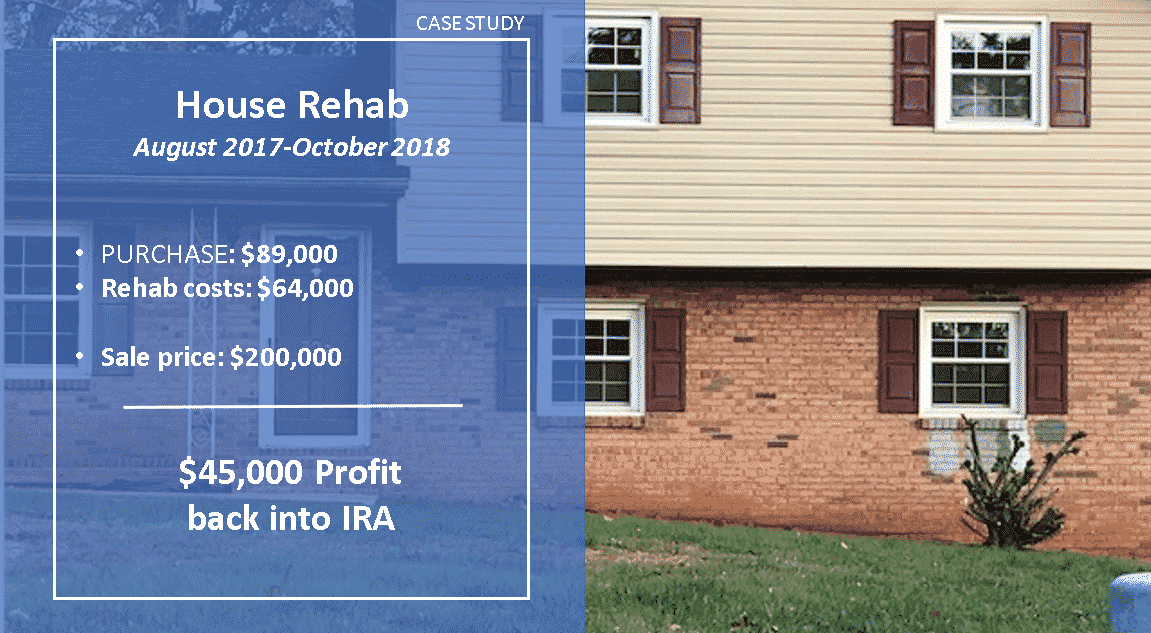

John: Absolutely. So of course, getting into the good stuff here. The rehab costs $64,000, it sold for approximately $200,000, and Mark made a $45,000 tax-advantaged profit.

When I say tax advantaged, this was a Traditional IRA, correct, Mark?

Mark: Correct.

John: Okay, this is what we refer to as a “tax-deductible” or “tax-deferred” account. So, when money was going into there from his contributions or 401(k) contributions, he was receiving tax deductions.

It’s growing tax-deferred and eventually when Mark begins withdrawal of the money, you would pay ordinary income taxes. But the advantage, of course of an IRA is that it’s tax-exempt in the year in which you have that income coming back in.

Hypothetical Example:

Let’s take a look if that $45,000 profit was outside of Mark’s IRA environment or IRA account. Let’s say he had a 20-percent effective tax on that $45,000 profit.

If we do that math, that’s close to $9,000 in taxes. Now, that’s just a hypothetical scenario.

But if you look at ordinary income tax rates on short-term capital gains $45,000, if I had a 20-percent effective tax rate, let’s say state and federal that’s close to $9,000 in taxes. This $45,000, because it’s in an IRA, is captured in that retirement plan and it’s exempt from taxation.

So $45,000 in profit, Mark on the sale of that property, take us through how that process worked for you.

Mark: It was very similar to the whole rehab itself and purchasing it. When I had the contract, we actually sent all the paperwork to Equity Trust to review and make sure that everything was fine.

The only issue was getting the closing attorney’s information so we could actually receive the wire transfer. And once we did all that, it was smooth.

John: Okay, that’s great. It’s important to note here that all that money is going directly back into the retirement plan.

1What types of accounts does Equity Trust hold?

Equity Trust holds a variety of IRAs, as well as other self-directed accounts, including:

- Traditional IRA

- Roth IRA

- SIMPLE IRA

- SEP IRA

- Solo 401(k)

- Roth Solo 401(k)

- Health Savings Account (HSA)

- Coverdell Education Savings Account (CESA)

2When I sell a property owned by my IRA, may I keep a portion of the proceeds and send the remaining portion to Equity Trust?

No. All income generated from the sale of a property owned by your IRA must be deposited directly into your IRA.

3Can my IRA purchase real estate that I currently own?

No. This is considered a prohibited transaction (see IRC 4975). You may not purchase a property, or interest in a property, that’s currently owned by a disqualified person, which includes yourself.

Case studies provided are for illustrative and educational purposes only. Past performance is not indicative of future results. Investing involves risk, including the possible loss of principal. Quotes and information included in the case studies and testimonials were provided by the investors and included with permission. Equity Trust Company does not independently verify all information provided by third parties.