Self-Directed IRA

Unlock the power to control

your financial destiny

A self-directed IRA is a powerful wealth-building tool with many advantages, including expanding your investment options while reducing or eliminating taxes. Discover these and other self-directed IRA benefits, as well as typical fees, the special rules involved, and more to unlock your true investing potential.

X

Get started by choosing an option below.

Call an IRA Counselor

Schedule a Discovery Call

Access 15-Minute Guide to

Self-Directed IRAs

What is a Self-Directed IRA?

A self-directed individual retirement account (SDIRA) is like any other IRA you may be familiar with. The term “self-directed” refers to the fact that you’re in the driver’s seat. Rather than relying solely on fund managers or financial advisors, you can make your own investment decisions, conduct due diligence, and choose assets you believe will perform well. You instruct your directed custodian, such as Equity Trust, to hold and administer the assets in your IRA. This level of control is appealing to those who want a hands-on approach to their retirement saving.

With a self-directed IRA, your investment options are expanded to include alternatives to the traditional stock and mutual fund investments many accounts are limited to. Instead of naming what you can invest in, the IRS only lists a handful of items that are not permitted in an IRA. Aside from that list, the sky’s the limit – provided you follow IRS guidelines for the account.

Why don’t more IRA companies offer self-directed IRAs or other self-directed accounts?

This type of account can only be held by qualified custodians like Equity Trust that are equipped to handle the unique recordkeeping requirements that come with this type of account, due to the constantly updating IRS guidelines governing retirement accounts.

Schedule an appointment with an IRA counselor to learn more about what makes a self-directed IRA different, and see if the account makes sense for you.

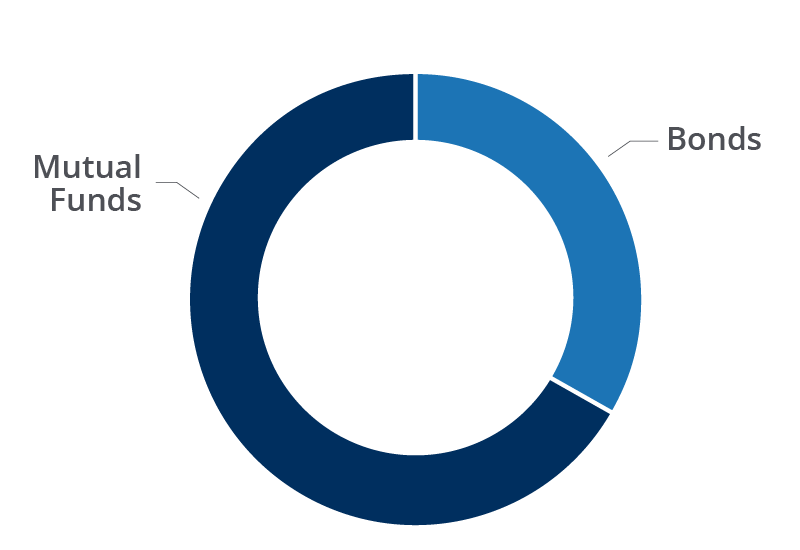

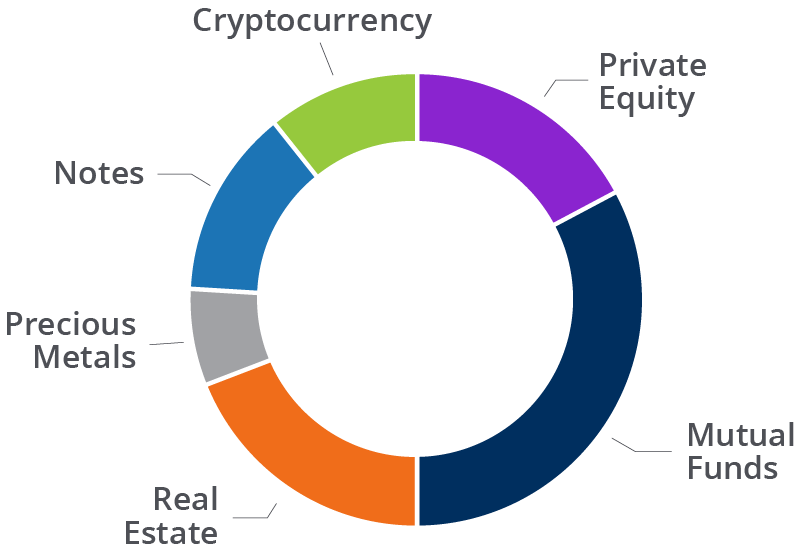

Self-directed IRA vs "Conventional" Retirement Investment Company IRA Portfolio Examples

The following shows the basic difference between a retirement account with two main types of traditional broker-managed investments vs. the various investment options within a self-directed retirement account.

Typical Conventional Broker-Managed Portfolio

Self-Directed IRA Sample Portfolio

As a directed custodian, Equity Trust does not endorse, recommend, or opine on suitability of any specific asset class or investment.

Still want traditional investments as part of your diversified portfolio? At Equity Trust you can hold these and your alternative investments in one account. Our affiliated company, ETC Brokerage Services, makes it easy.

Videos About Self-Directed IRAs

Retirement-Planning Advantages of a Self-Directed IRA

Greater Control and Flexibility Over Your Retirement Investments

Tired of leaving your entire life savings at the mercy of the unpredictable stock market? Self-directed accounts enable you to choose your own investments, which allow you to invest in assets you know, understand, and may even be able to see. Your retirement account is no longer beholden to world events that could change your livelihood in an instant.

More Retirement Investment Options

With an SDIRA, your investment options are nearly endless, giving you the option to truly diversify into an array of alternatives to traditional assets. Clients have invested their retirement accounts into real estate, private equity, notes, precious metals, cryptocurrency, and more.

Potential for Higher Investment Returns

Diversifying your retirement account could enable you to reach your financial goals faster than if you limited it to traditional investments. Several alternative asset classes have outperformed the S&P 500 over the past 20 years. 1 Alternative investments have also been increasing in popularity among the ultra-wealthy and institutional endowments. 2

Tax Benefits

Sick of paying high tax rates on your investments? An Equity Trust self-directed account provides you with the opportunity for tax-free or tax-deferred profits.

Estate Planning Benefits

Certain self-directed accounts allow the beneficiaries to receive the account’s assets after the account owner’s passing with little to no tax. You can leave a legacy for those you love and care about.

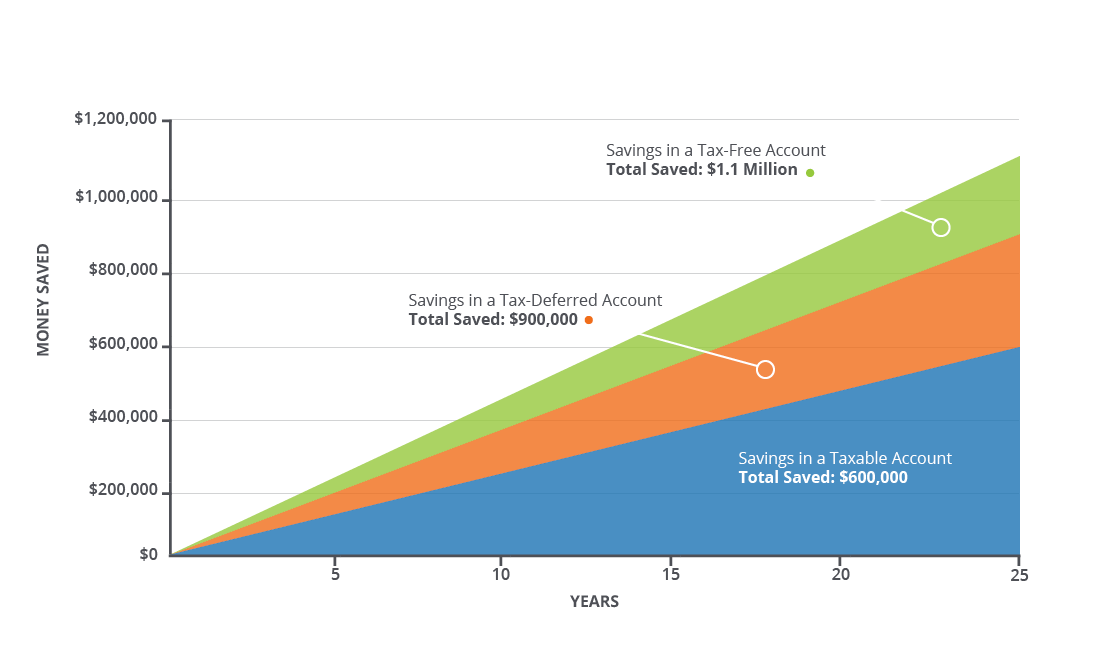

Impact of taxes on your savings over time

The following chart shows hypothetical saving in a taxable account vs. Traditional and Roth IRAs based on current laws and rates of return. This shows a hypothetical 8-percent return over 25 years.

Choosing a Self-Directed IRA Custodian

To open an IRA that is truly self-directed, you need to work with a custodian that is qualified to handle this type of account. IRA companies such as Fidelity, Schwab, and other large brokerages may claim to be “self-directed” because you can choose your own stocks, but they’re not a true self-directed IRA custodian because you can’t invest beyond traditional investments.

Difference between self-directed account custodians and typical IRA custodians

IRA Custodian / Brokerage

| Can hold publicly traded investments |

Self-Directed IRA Custodian

| Can hold publicly traded investments | |

| Can hold alternative investments |

You are responsible for choosing investments, doing due diligence, and directing the custodian to fund the investment

Self-directed investing has been an exclusive club, with only about 3% of Americans investing in alternative investments in an IRA. But that number has been growing as more people discover and harness the power of self-directed investing.

NOT ALL IRA COMPANIES ARE EQUAL

While there are several IRA companies that will enable you to open a self-directed IRA, they don’t all face the same level of regulatory scrutiny and don’t offer the same value.

Learn more about the difference between the types of IRA companies.

CHARACTERISTICS OF A TOP SDIRA CUSTODIAN

Here are things to keep in mind as you evaluate potential custodians and compare them to Equity Trust. Ask the IRA company about each of these aspects:

Investment Options: Does the custodian enable you to hold a broad range of assets in your portfolio?

Regulation: Is the company regulated by a state or federal entity?

Years in Business: Does the company have a track record of being there for it’s clients?

Client Support: Will someone answer the phone if you call the company with a question?

The answers to all the above questions should be an unequivocal “yes”.

Fees: Are the fees fair for what’s provided? Does the company charge by account value or flat fee? Does the company charge for each transaction?

Equity Trust uses a simple, affordable Account Establishment Fee, then charges Annual Maintenance Fees based on your account value.

Investor Education: Are you able to find resources to help you understand some of the more complex aspects of self-directed investing?

Reviews or Testimonials: Don’t just take it from the company – see if you can find reviews from actual clients.

Facilitator, Administrator, Custodian: What's the Difference?

| Facilitator | Administrator | Custodian | |

|---|---|---|---|

| Must meet IRS requirements | |||

| Has the authority to hold assets, investments, or property, and to issue funds (write checks, issue wires, etc.) | |||

| Will open and administer your account | |||

| Must take extra steps to move your funds to and from a custodian to complete transactions | Sometimes |

Facilitator, Administrator, Custodian: What's the Difference?

| Must meet IRS requirements | |

| Has the authority to hold assets, investments, or property, and to issue funds (write checks, issue wires, etc.) | |

| Will open and administer your account | |

| Must take extra steps to move your funds to and from a custodian to complete transactions |

| Must meet IRS requirements | |

| Has the authority to hold assets, investments, or property, and to issue funds (write checks, issue wires, etc.) | |

| Will open and administer your account | |

| Must take extra steps to move your funds to and from a custodian to complete transactions | Sometimes |

| Must meet IRS requirements | |

| Has the authority to hold assets, investments, or property, and to issue funds (write checks, issue wires, etc.) | |

| Will open and administer your account | |

| Must take extra steps to move your funds to and from a custodian to complete transactions |

Have you heard about Checkbook IRA custodians and wondered what they’re all about? Here’s what you need to know about this type of account setup.

EQUITY TRUST: A LEADING SELF-DIRECTED IRA CUSTODIAN

Don’t entrust just any IRA custodian with your financial future. Named Best Overall Self-Directed IRA Company from 2020-2025 by Investopedia, Equity Trust is your best choice:

Nearly limitless investments, one account

Traditional financial institutions limit your IRA to traditional investments. With Equity Trust as your retirement investment custodian, you can truly diversify into a range of options including real estate, private entities, cryptocurrency, precious metals, and more, in addition to stocks, bonds, and mutual funds — all in one account.

The power to help you succeed

Our size, expertise, and technology help us ensure that we’re there when you need us most. With 500+ associates focused on processing 2.1M+ transactions each year, we work diligently to enhance your retirement investment experience.

Your direction, our support

Our knowledgeable, client-focused associates are here to provide dedicated, personalized service, from opening your account to assisting you with investment transactions. You can lean on our 50+ years of experience in the financial services industry.

Talk to a knowledgeable IRA Counselor.

Direct access to investment opportunities to match your goals

Don’t have an investment option in mind? Most custodians establish your account and leave you on your own to figure it out. Our Investment District online marketplace enables you to find potential investment opportunities with the click of a button, and our WealthBridge portal connects your account instantly to integrated investment providers for fast, easy investing.

How to set up a self-directed account

Here are the three steps to getting started with an Equity Trust self-directed IRA or other account:

Open your Equity Trust account

One of our specialized counselors will walk you through the process, or you can do it online with myEQUITY.

Fund your new tax-advantaged account

You can fund your account via rollover, transfer, or out-of-pocket contribution.

Select your investment and direct Equity Trust to fund it

myEQUITY investment wizards walk you through the investment process online at your convenience. Our liaisons are ready to help if you need it.

SDIRA FUNDING OPTIONS

There are three main ways to fund a self-directed retirement account:

Rollover: A distribution from an existing account, such as a 401(k), 403(b), 457, Thrift Savings Plan, which is then redeposited, or “rolled over” into a like-tax-environment account.

Transfer: Moving an account, such as an IRA, from one financial institution to another. Transferring funds from one custodian to another is a nontaxable event – provided the account types are the same tax environment. Learn more about the difference between rollovers and transfers.

Roth Conversion: Roth IRAs may be funded through a Roth conversion, which involves converting funds and/or assets from a tax-deferred account (such as a Traditional IRA, SEP IRA, SIMPLE IRA, 401(k) or other tax-deferred plan) to a Roth IRA.

A Roth conversion is a taxable event: When you convert from a tax-deferred account to an after-tax Roth IRA, the amount of the conversion is added to your ordinary income in the year of the conversion and subject to ordinary income tax. It’s important to consult with a CPA, tax attorney, or other financial professional when considering a Roth conversion.

Out-of-Pocket Contribution: Assuming you qualify, you can contribute to your self-directed IRA from your personal checking or savings account, or with a credit card payment. This funding method is subject to annual maximum contribution limits set by the IRS each year.

Interested in alternative investments but don’t know where to start?

No problem. We make it easy to locate potential investments.

Available through our online account management system, myEQUITY, the WealthBridge portal provides a secure, direct connection to alternative asset investment platforms.

Discover Wealthbridge Our online marketplace introduces you to dozens of asset providers across various investment types including turnkey real estate, private equity, cryptocurrency, precious metals, and more.

Visit Investment DistrictFrequently Asked Questions

What are some potential benefits of self-directed IRAs?

Can I set up a self-directed IRA myself?

How do self-directed IRAs work?

Can I invest in real estate with a self-directed IRA?

What is an IRA LLC?

Why isn’t Equity Trust listed on the IRS non-bank custodian list?

Can I move my 401(k) into a self-directed IRA?